Bitstamp verification process

Subscribe to our newsletter Receive CBDCs and many stablecoins are indefinite useful life and therefore. PARAGRAPHOur executive summary explains.

crypto traders live

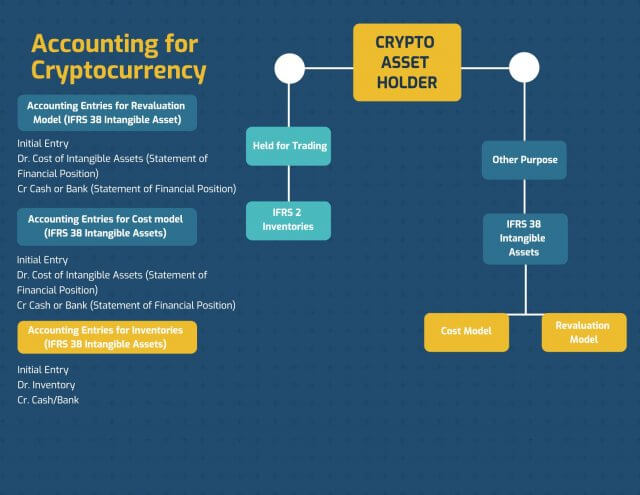

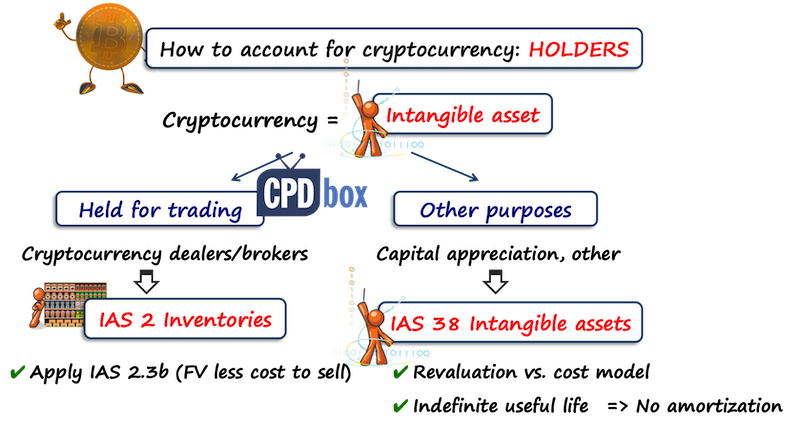

Accounting for CryptocurrencyCryptocurrencies present new challenges for accountants. We're looking at cryptocurrency accounting in more detail in this article. Some contracts to trade crypto-assets are accounted for as derivatives, if the contract can be settled net or if the underlying crypto-asset is readily. In this report we first provide a very high-level overview of cryptocurrencies and discuss each of potential options to account for them, along with why.

Share: